A falling dollar generally supports a rise in stocks

Key points:

- The 26-week rate of change for the Dollar Index (DXY) shifted from above 3% to below -0.5%

- Comparable reversals in the dollar preceded excellent returns for the S&P 500 over the next year

- Commodities and gold saw gains, while long-term yields decreased as the dollar remained stable a year later

An additional macro factor offers further support for rising stock prices

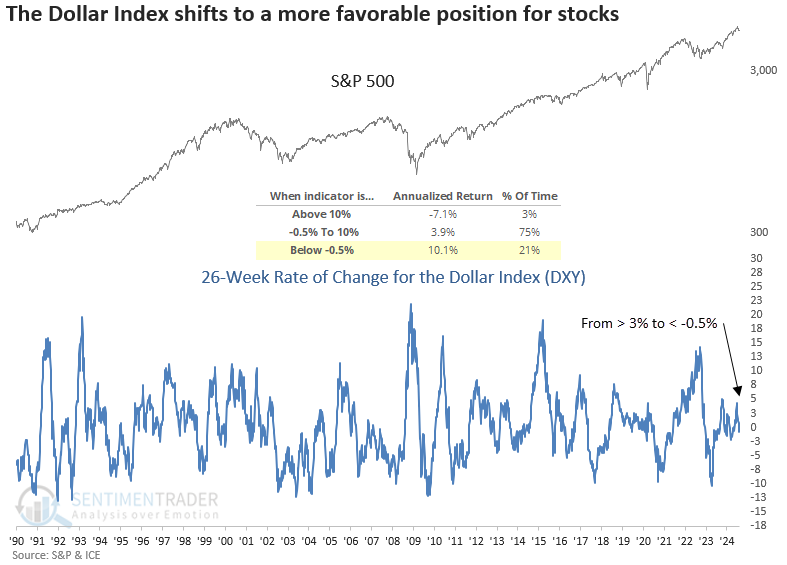

A weaker dollar enhances the global competitiveness of U.S. exports and boosts the earnings of multinational companies. Over the past 26 weeks, the U.S. Dollar Index (DXY) has gradually declined, signaling a potentially more favorable climate for equities. This downturn in the dollar, coupled with lower interest rates, offers a supportive foundation for the stock market.

As illustrated in the chart below, since 1972, the S&P 500 has generated an annualized return of 10.1% when the 26-week rate of change dips below -0.5%, a marked difference compared to when it surpasses 10%.

The previous downshift in the Dollar Index (DXY) occurred in November 2023, leading to an 11% gain in the S&P 500 over the subsequent six months.

Comparable shifts in the Dollar Index (DXY) preceded excellent returns

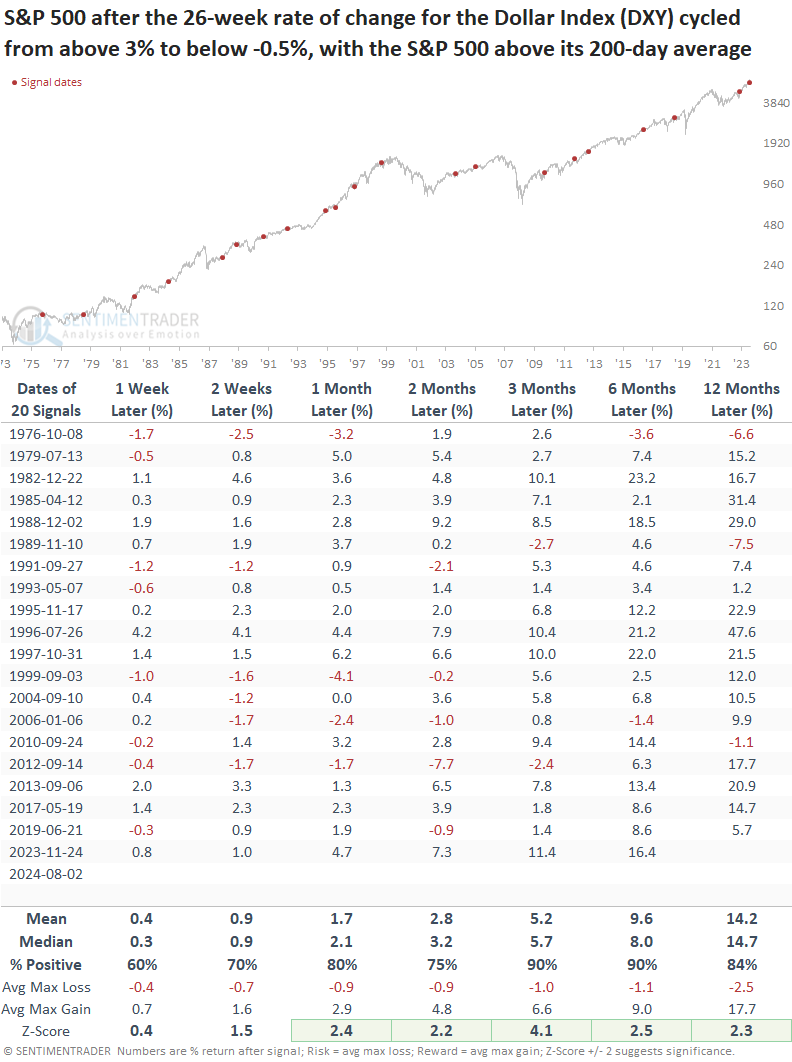

Whenever the 26-week rate of change for the Dollar Index (DXY) cycled from above 3% to below -0.5%, with the S&P 500 above its 200-day average, the world's most benchmarked index rose 90% of the time over the subsequent three and six months. Additionally, the index displayed significance relative to random returns from one to twelve months later.

Bottom line: The dollar is a critical factor for stocks.

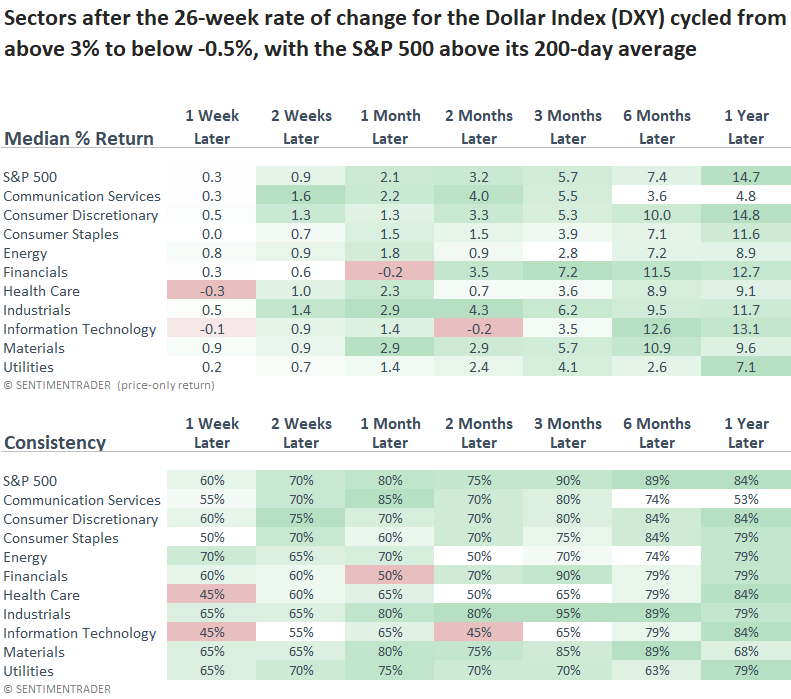

While there is no clear-cut winner from a sector perspective, companies with a large multinational presence generally tend to benefit when the dollar provides a tailwind.

Other asset classes

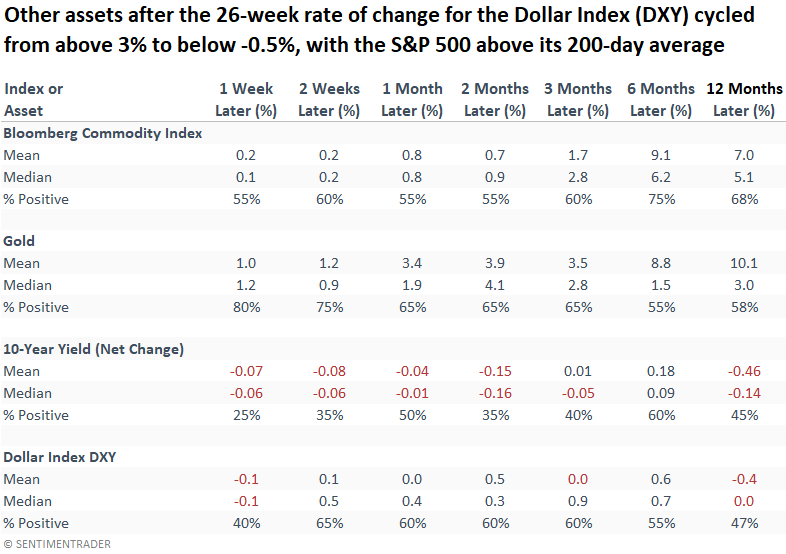

After the Dollar Index (DXY) declined, the basket of currencies showed a mild upward trend over the next six months, though it remained largely unchanged after a year. This period of dollar stability proved advantageous for commodities and gold. Meanwhile, the 10-year Treasury yield consistently declined, providing support for stocks.

What the research tells us...

The easing of capital costs (10-year Treasury yield down 75 bps since April) for companies and consumers, coupled with a lower dollar index, is setting the stage for a bullish backdrop for stocks once the current correction ends, provided the economy doesn't nosedive from its current growth trajectory of 2.9% based on the latest Atlanta Fed GDPNow forecast. Following comparable shifts in the Dollar Index (DXY) with the S&P 500 in a long-term uptrend, the world's most benchmarked index displayed excellent returns and consistency over the subsequent year. Commodities and gold could trend higher with the dollar reversing from a headwind to a tailwind.