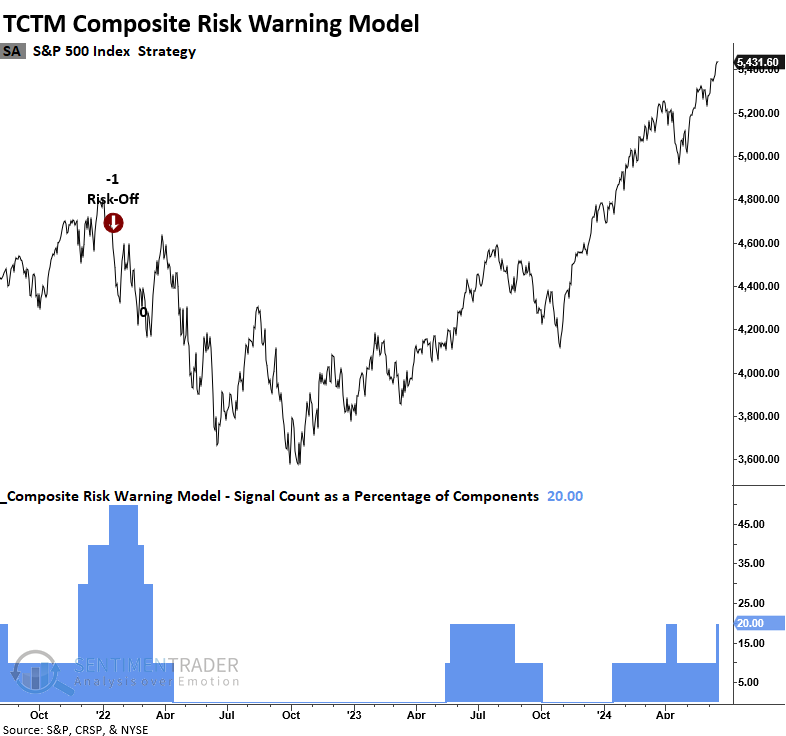

A Composite Risk Warning Model member triggered an alert

Key points:

- The ratio between 52-week highs and lows on the NYSE exceeded -1.5 to 1, two sessions or fewer from a high

- Similar skews in highs versus lows preceded negative returns for the S&P 500 over the subsequent two months

- The TCTM Composite Risk Warning Model signal count increased to 20%

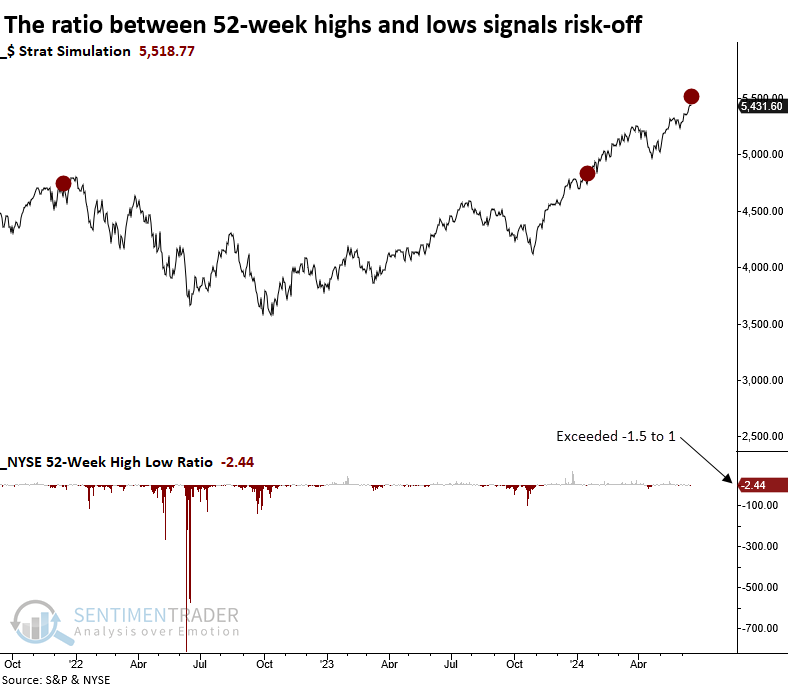

NYSE 52-week lows exceeded highs, with the S&P 500 near an annual high

A model that monitors NYSE 52-week highs relative to lows exceeded a ratio of -1.5 to 1, with the S&P 500 two days or fewer from an annual high, triggering a risk-off signal from a member in the TCTM Composite Risk Warning Model.

The previous alert, which occurred in January 2024, was a standalone event, highlighting why no indicator or model should ever be used in isolation. A weight-of-the-evidence approach is always preferable.

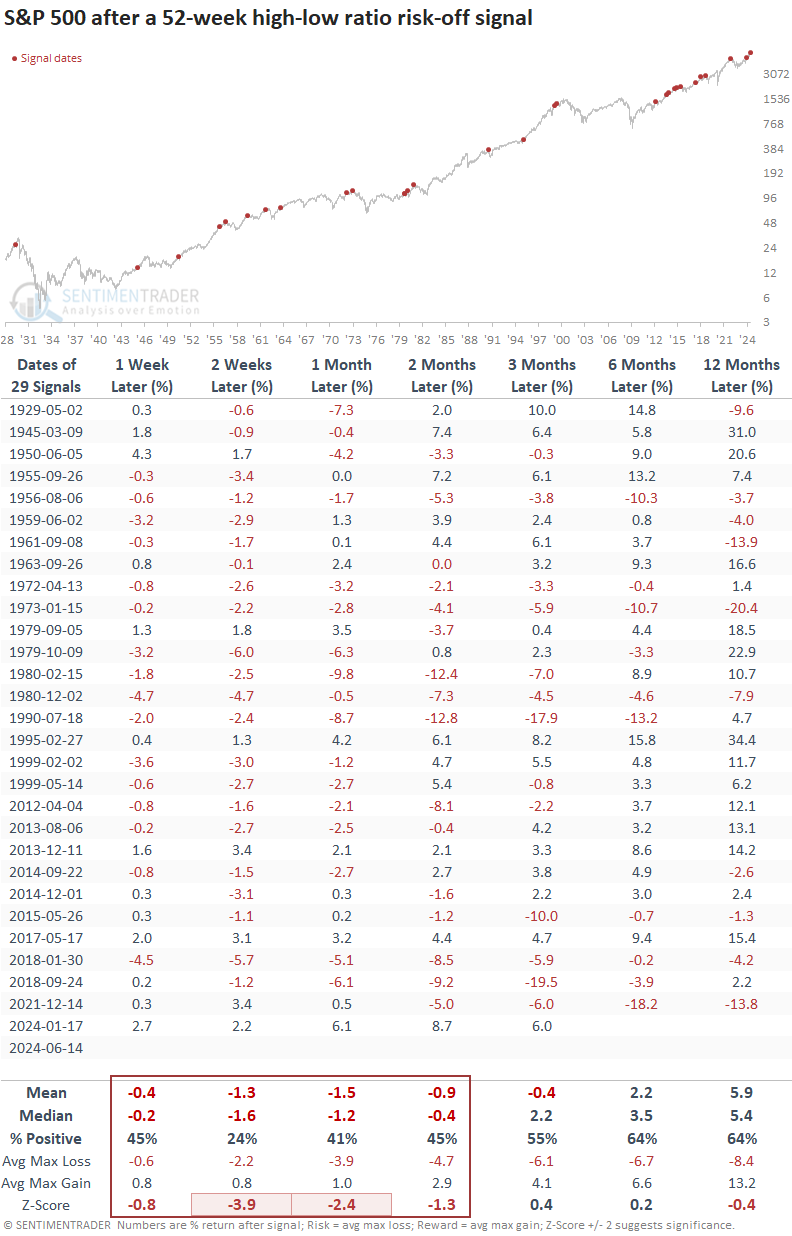

Comparable skews in 52-week highs versus lows preceded negative returns

Should the NYSE 52-week high-to-low ratio exceed -1.5 to 1 in two days or fewer of the S&P 500 reaching an annual high, the world's most benchmarked index has historically shown negative returns and unfavorable win rates over the next two months. The first two weeks exhibited the highest risk, with the index declining 76% of the time.

While longer-term horizons were favorable, the results were uninspiring relative to history.

The weight of the evidence has not overwhelmingly turned unfavorable

The Composite Risk Warning Model requires a minimum composite signal count of 50% to activate an alert, a threshold that has yet to be achieved.

What the research tells us...

Over the last few weeks, our research has highlighted an increasing number of stock participation problems across different indexes and exchanges. Until now, most warnings have been mainly from short-to medium-term indicators. However, a new alert from a TCTM Composite Risk Warning Model member, which compares 52-week highs to lows, suggests risks are rising. Similar alerts tended to result in an unfavorable outlook for the S&P 500 over the subsequent two months. Should the list of items on the bearish side of the ledger expand further, investors would be wise to heed the market's message.