A bullish and bearish message in corporate bonds

Key points:

- Price trend and breadth-based indicators for investment-grade bonds turn bullish

- After similar conditions, investment-grade bonds showed solid long-term results

- A trading system that uses market breadth indicators issued a sell signal for high-yield bonds

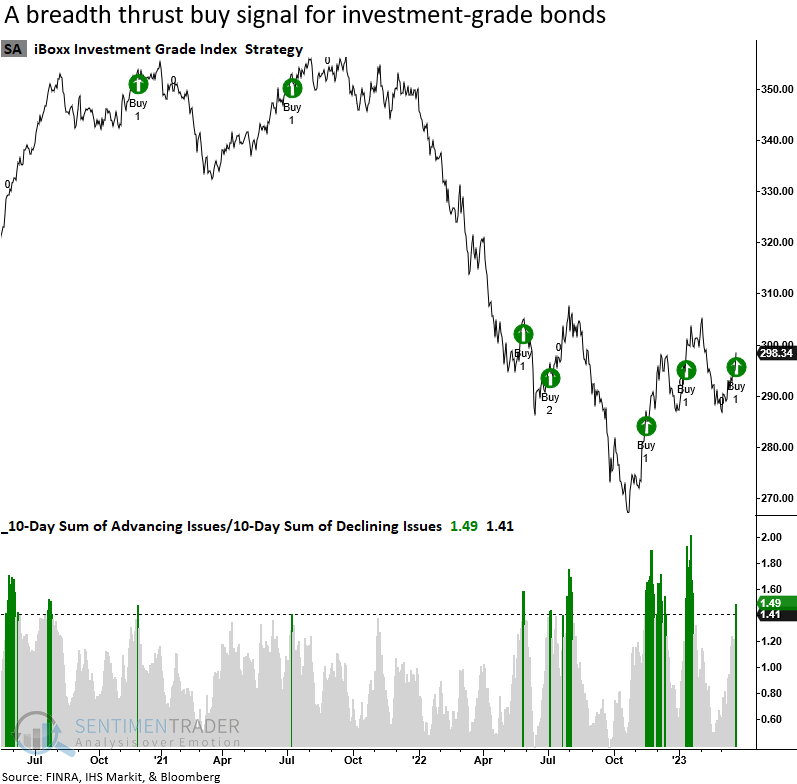

Investment-grade bonds surge higher as interest rates tumble

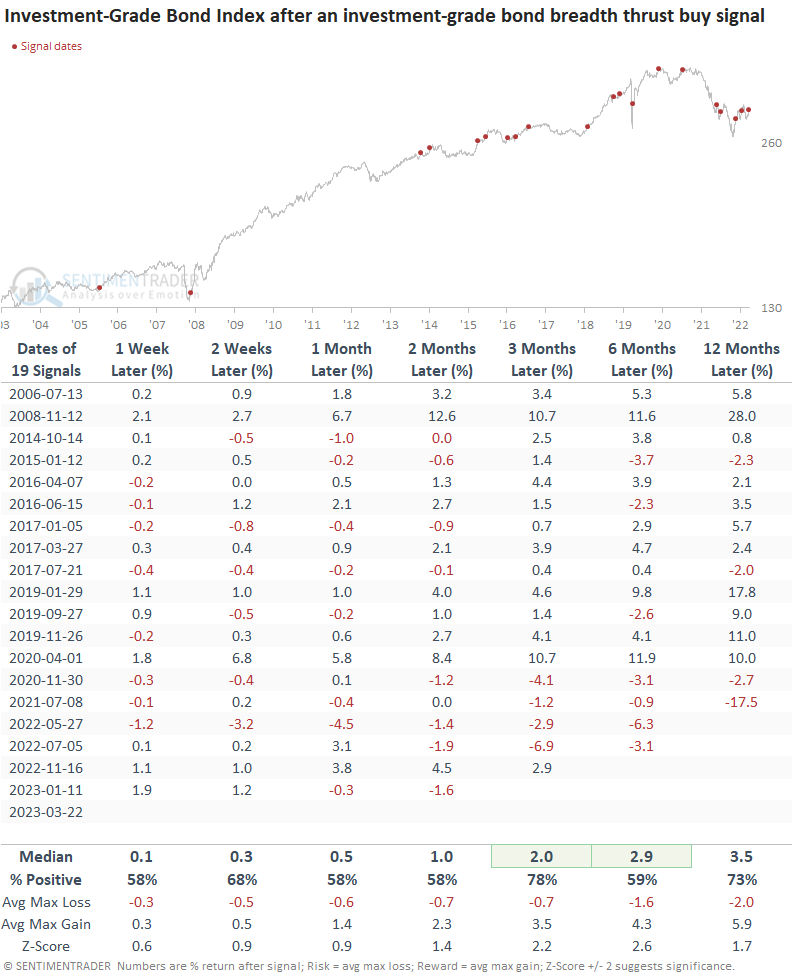

The recent reversal in Treasury yields from uptrends to downtrends sent investment-grade bond prices surging again, triggering the 5th breadth thrust buy signal in the last ten months. While 3 out of 4 previous alerts showed a gain at some point in the first month, the increased upside participation did not materialize into a long-term trend change for an investment-grade bond index until now.

From a subjective perspective, the investment-grade bond index chart looks like a bullish inverse head and shoulders pattern could be forming.

Similar surges in participation preceded positive returns

When a breadth thrust signal triggers for investment-grade bonds, the iBoxx IG Index shows a clear upward bias across all time frames. The sweet spot occurs three months later, which offers a solid win rate and z-score.

While the breadth thrust provides a short-term money-making opportunity for traders, the signal can give investors an early heads-up of a potential long-term trend change. After one of the worst years in history for bond investors, a bullish trend change would be a welcome development.

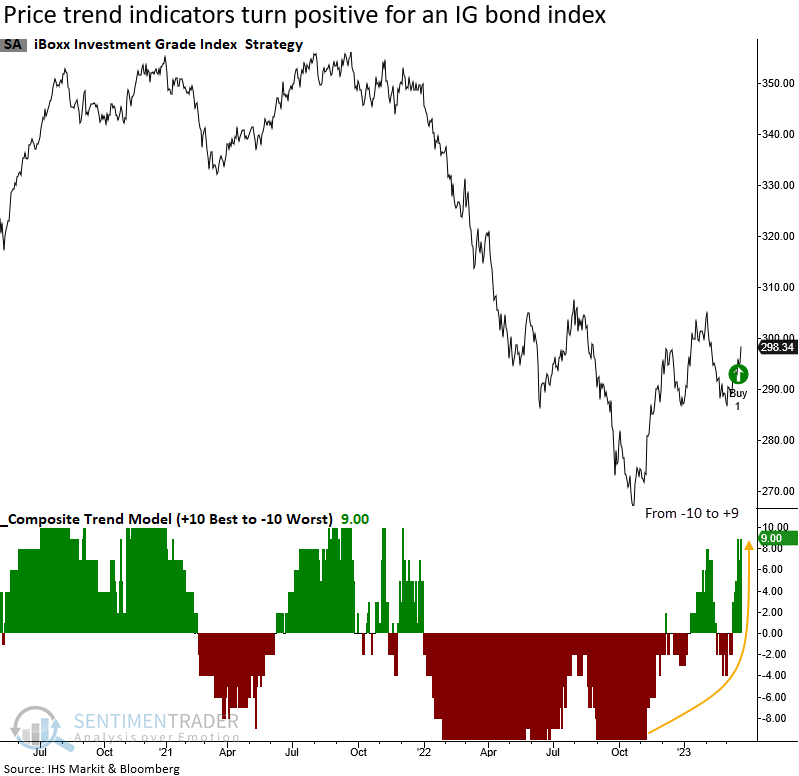

What's different this time

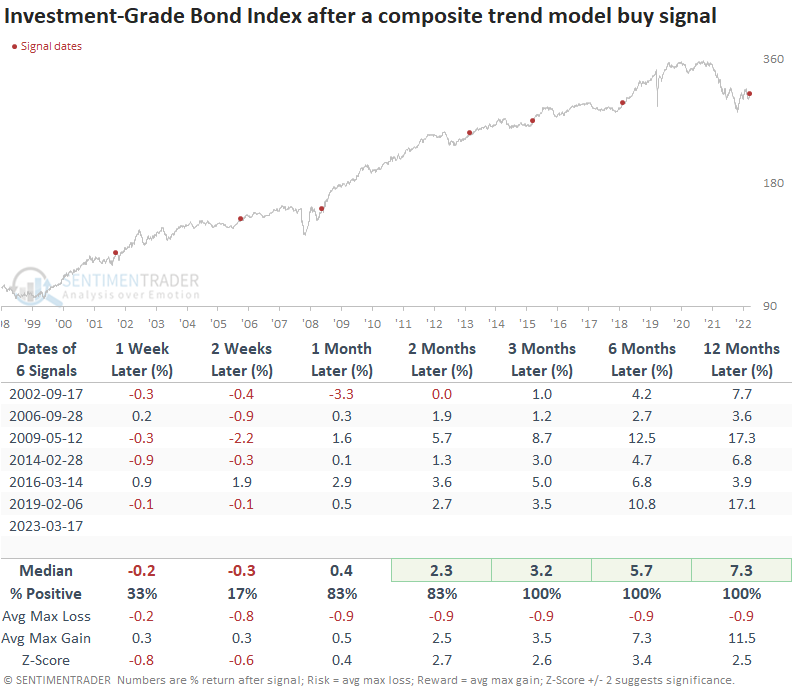

Over the last ten months, the cluster of breadth thrusts slowed the extreme downside momentum in the iBoxx Investment-Grade Bond Index. In doing so, price-based indicators bottomed and have now turned up, lifting a composite trend model to the second-best score possible.

When the composite score cycles from -10 to +9, like now, investment-grade bonds tend to rally.

While the sample size is small due to the limited history of the iBoxx IG index, it's hard to argue with the long-term results. And even though the trend change system did not get tested in a high-inflation environment like the 1970s, it did successfully navigate two brutal equity bear markets.

A conflicting message from corporate bonds that are more economically sensitive

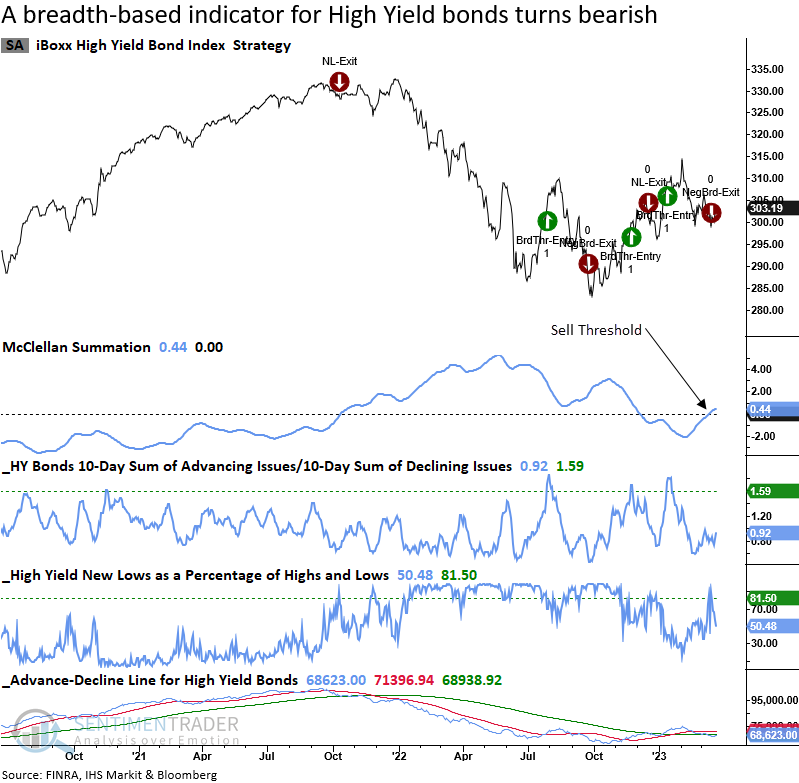

A trend-following system for high-yield bonds recently triggered a risk-off alert when one of the breadth-based indicators, the McClellan Summation Index, crossed the sell-signal threshold. The diverging signals between higher and lower-quality corporate bonds are worth noting because high-yield bonds are more sensitive to economic/credit conditions.

So, we must be mindful that high-yield bonds could foreshadow a further slowing in the economy, which would not be bullish for risk assets.

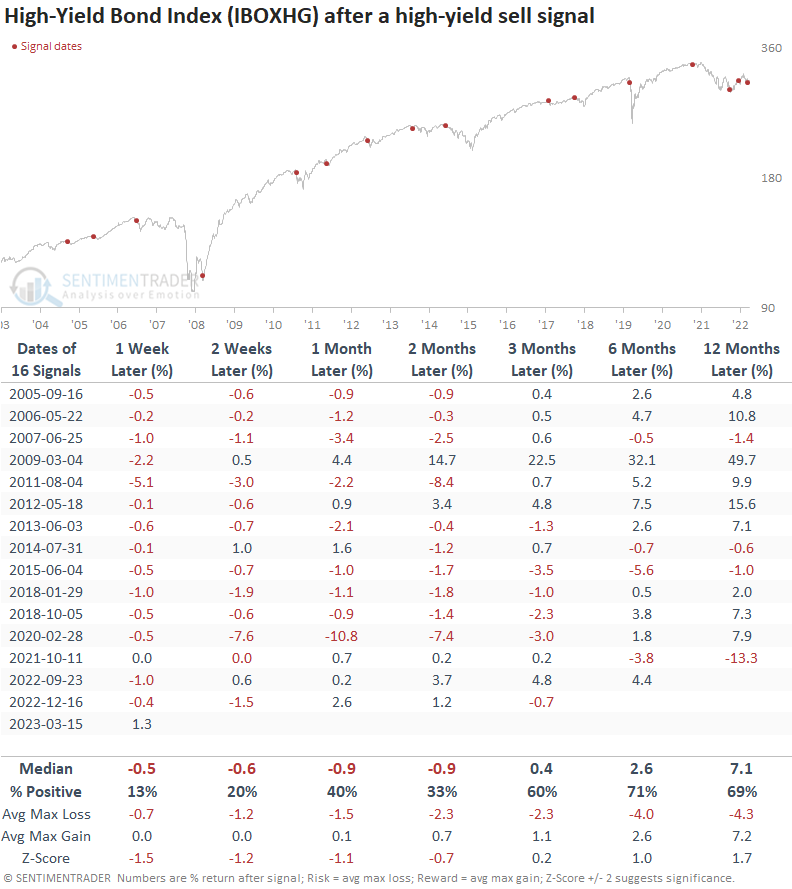

Similar sell signals for high-yield bonds preceded negative returns

When the breadth-based high-yield trading system registers a sell signal, returns and win rates over the next few months look troubling, especially in the near term.

What the research tells us...

Treasury yields declined significantly in the last few weeks, sending investment-grade bonds surging. The increased upside participation triggered a breadth thrust signal with bullish implications for higher-quality corporate bonds. With a cluster of thrust signals stabilizing corporate bond prices over the last ten months, trend-following components in a composite model reversed higher, triggering a bullish trend signal for investment-grade bonds. While the outlook for higher-quality corporate bonds looks constructive, one can't say the same for lower-quality high-yield issues. We must be mindful of the market message with credit-sensitive high-yield bonds acting poorly.