A broken correlation between growth and value

Key points:

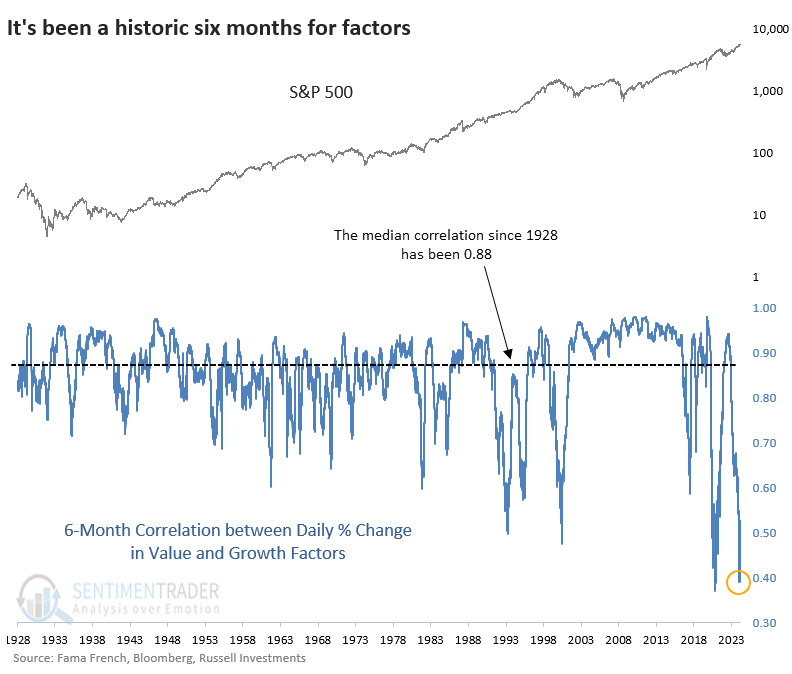

- Over the past 6 months, the correlation between value and growth stocks plunged to a near-record low

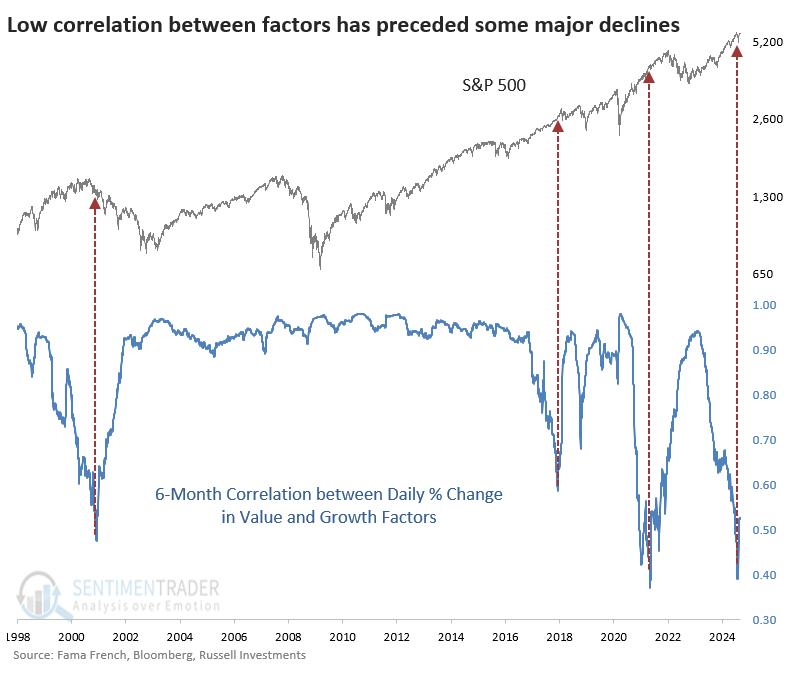

- Since 1998, a low correlation between those factors preceded significant stock market peaks

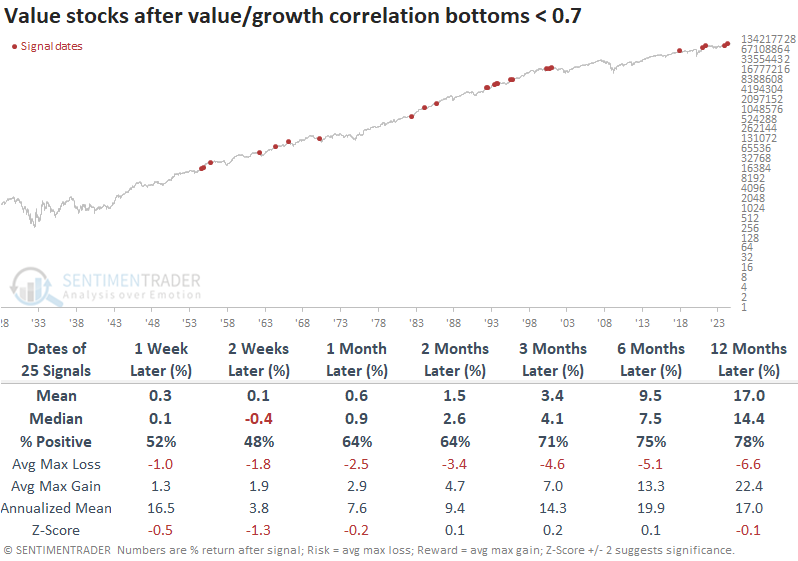

- A longer history shows it hasn't been quite this ominous of a signal, especially for value stocks

A broken relationship

It's no secret that the stock market has been disjointed this year. This was evident as early as January, but when small-cap cap stocks started to perk up, some of the divergences melted away.

One that did was the activity in value and growth stocks. Almost daily, one of those factors would rise while the other fell. That has preceded one of the lowest correlations over six months in nearly 100 years. The only time since 1928 when the correlation was lower was May 2021.

If we zoom in on the chart and look at the past 25 years, there is reason to be concerned. Each time the correlation deteriorated significantly, it preceded trouble in the S&P 500.

We try to be objective, however, and objectively, it's not quite that clear-cut.

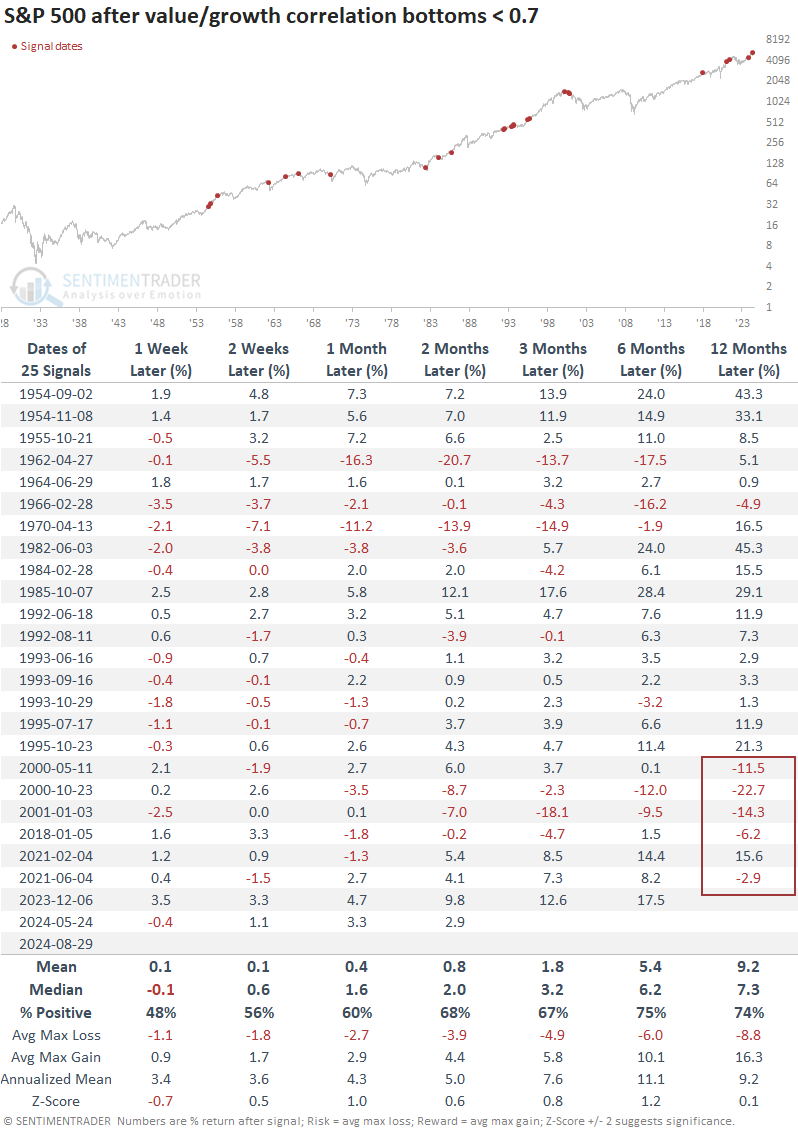

A good sign for value

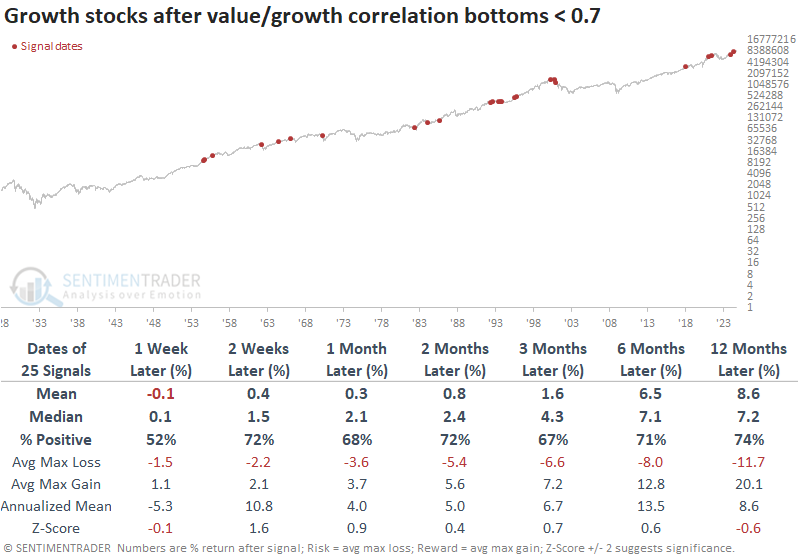

The table below shows each time since 1928 when the correlation between value and growth stocks bottomed below 0.7. The key word is "bottomed," and it's not fair to look at a chart to determine those points. We didn't know in real-time whether something was a bottom or not.

To make it more realistic, the table shows every time the correlation dropped below 0.7 and didn't make a lower low for one month. That's where we are now. Some of those did end up being the low for the cycle, but often did not; the correlation turned around and went to a lower low. Overall, it did not lead to dramatic trouble, except for one-year returns over the past 25 years.

These were decent signals for value stocks. The median return over the next year was +14.4%, nearly double the S&P 500's median return, with lower risk and higher reward.

Growth stocks tended to rise less often over the medium- to long-term, and their average return was about half that of value stocks. In the short run, however, growth stocks tended to benefit more than value. The switch occurred at around the three-month mark.

What the research tells us...

Finding a relationship that looks ominous on a chart over a specific time frame is easy. Several equity market peaks over the past 25 years have similar qualities, leading investors to extrapolate those to all peaks. Markets aren't that easy, however, which is evident when we look at longer data series with larger sample sizes.

When value and growth divergence as much as they have over the past six months, it hasn't been a consistent negative for stocks. The biggest caveat to writing it off entirely is that over the past 25 years, it has preceded trouble more often than not. So, we have to determine whether recent history is more relevant, and that's an individual decision. The biggest takeaway is likely that value stocks have tended to perform significantly better than growth stocks and the broader market after troughs in the value/growth correlation.