A big turn of events for the Nasdaq

Key points:

- The Nasdaq Composite suffered its largest loss in a year to a multi-month low but still in a long-term uptrend

- Similar shake-outs have preceded a significant short-term volatility, though with long-term positive returns

- Other indices and defensive-oriented stocks showed better returns with more consistency

A conspicuous loss

Dip-buyers haven't shown any great interest in stepping up, and that's an issue for a momentum-driven index like the tech-heavy Nasdaq 100. It may be less of a concern for broader indices like the Nasdaq Composite, especially when selling pressure has already been overwhelming.

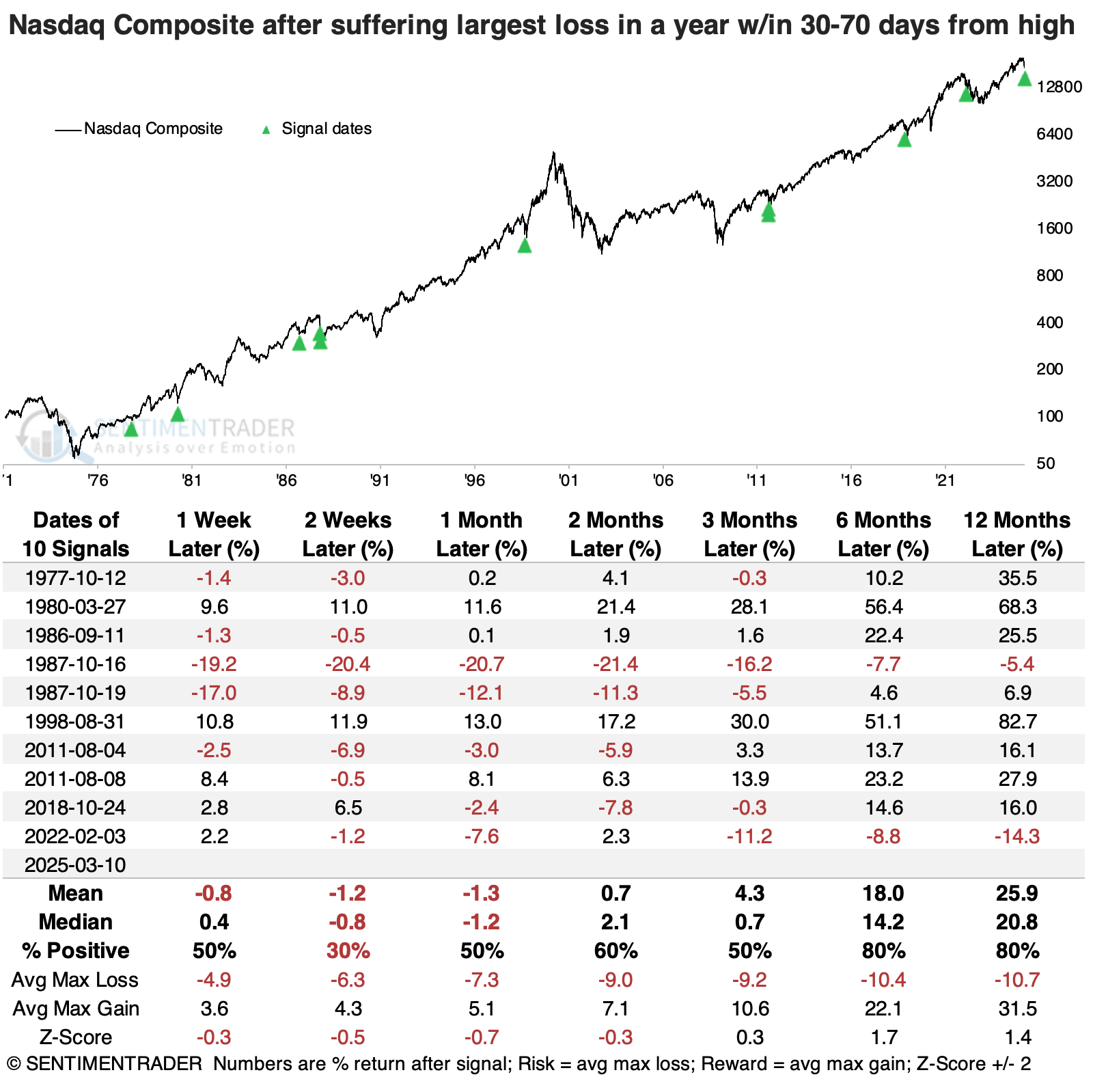

The Composite suffered its largest loss in over a year on Monday. This is moderately removed from its last multi-year high a few months ago.

Similar large losses, when removed from the last high within the past several months, have tended to precede more short-term losses but fewer longer-term ones.

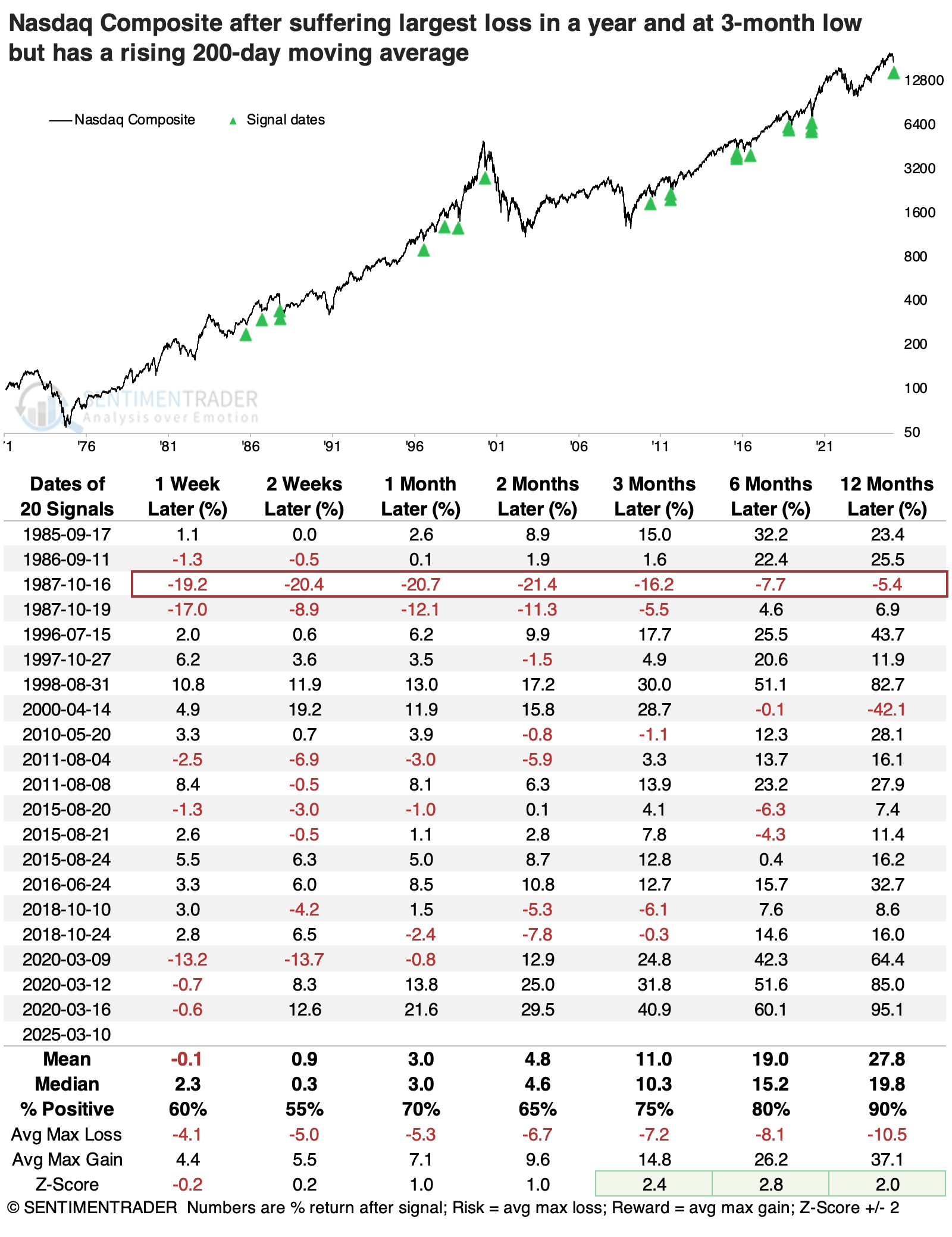

Adding more context to the move in the Nasdaq, its largest loss in a year occurred when the index was still above a rising 200-day moving average, but severe enough to push it down to a 3-month low. In other words, a panicky bout of selling to an intermediate-term low within a long-term uptrend.

These exact conditions were triggered right before the Black Monday crash of 1987, which is scary enough. Other than that, there were several further large short-term losses - these types of selling days tended to cluster somewhat (1987, 2011, 2015, 2018, 2020). Other than that one signal in 1987, the Nasdaq managed to show a positive return either three or six months later each time.

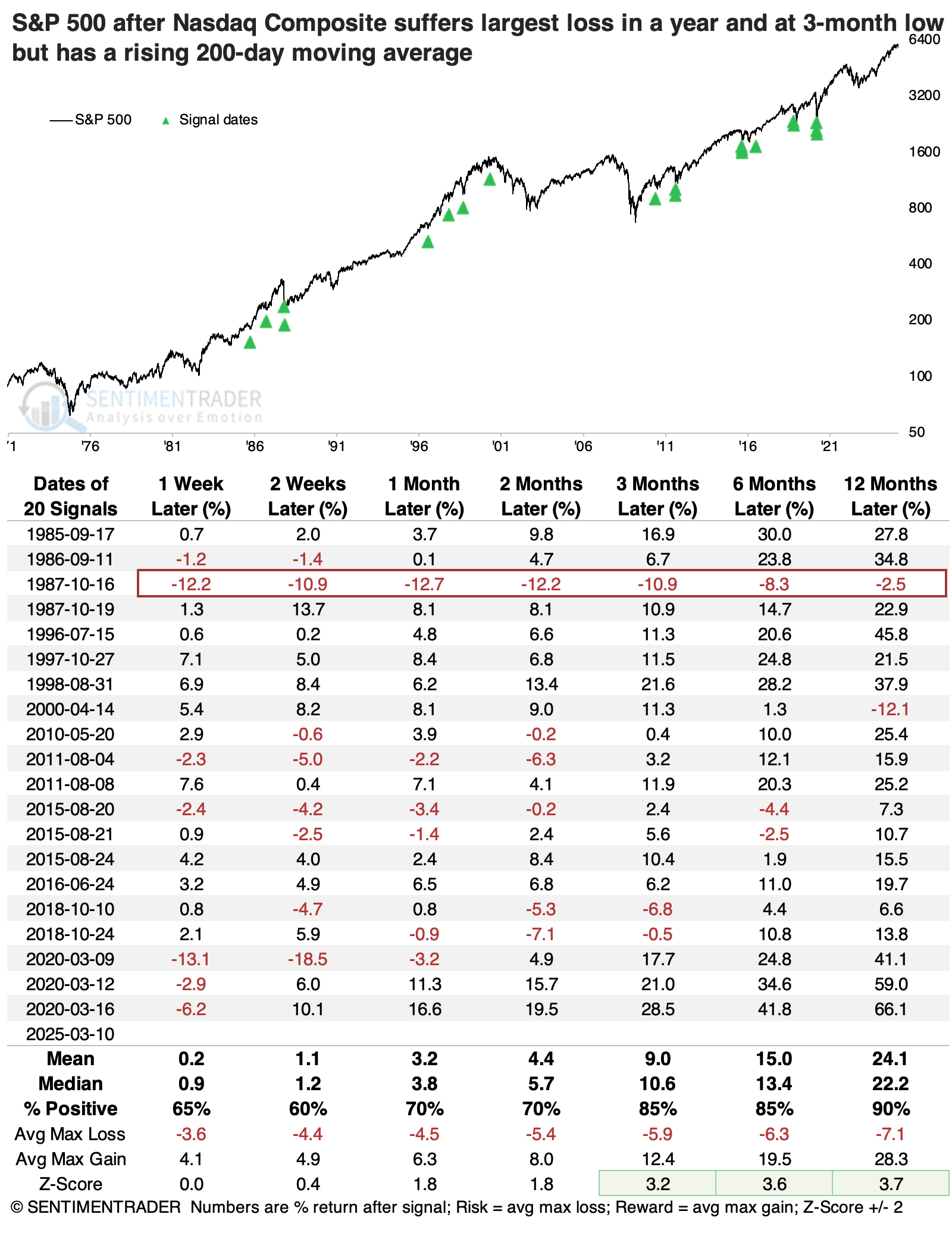

Better for other stocks

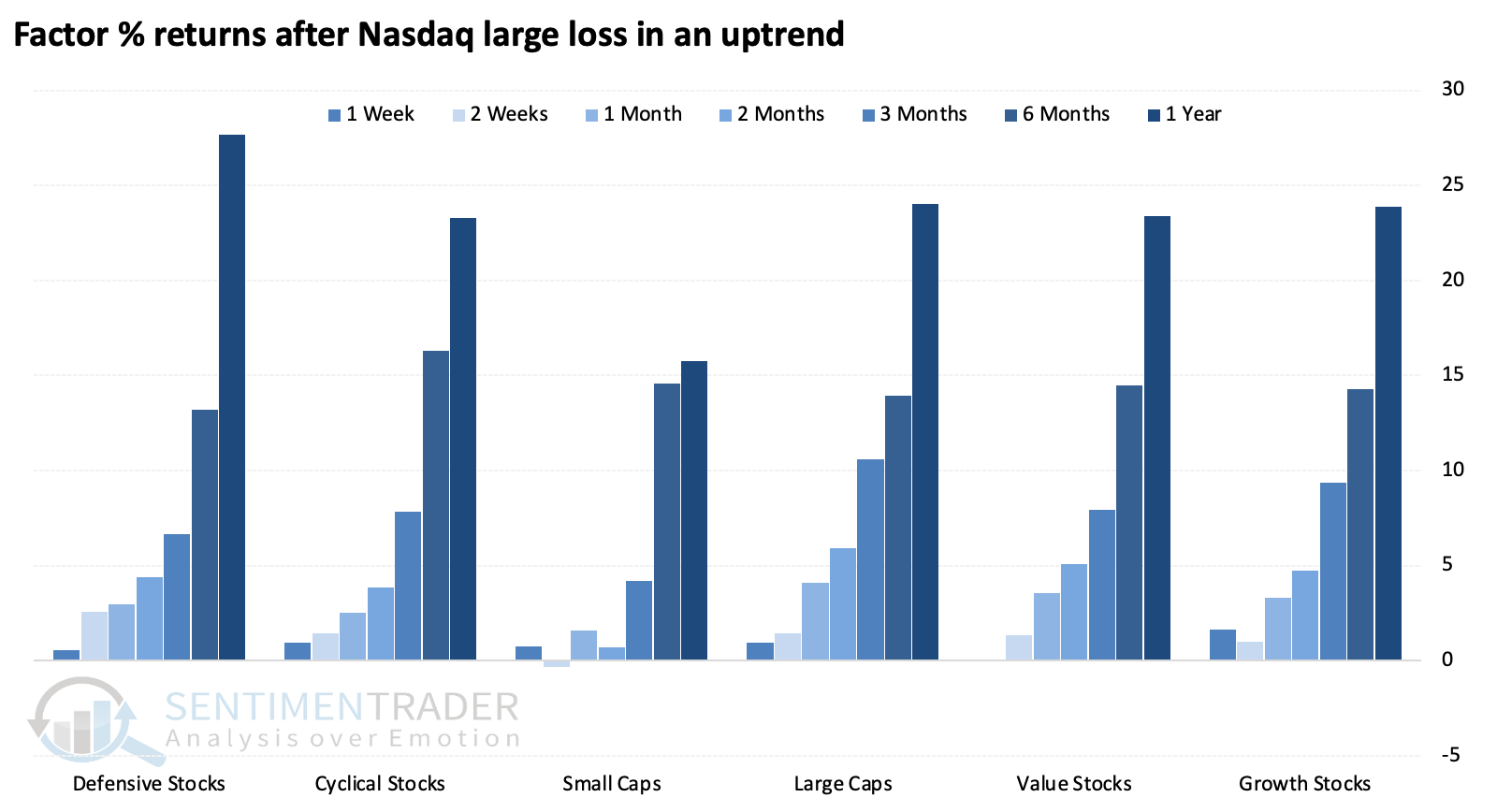

When investors violently soured on the generally poorer-quality companies in the Nasdaq, these mini-panics tended to serve investors well in more robust companies. The S&P 500 showed an excellent tendency to rebound over 3-12 months, except for that signal before Black Monday. Over the following year, it managed a higher median return than the Nasdaq, with less risk and almost as much reward.

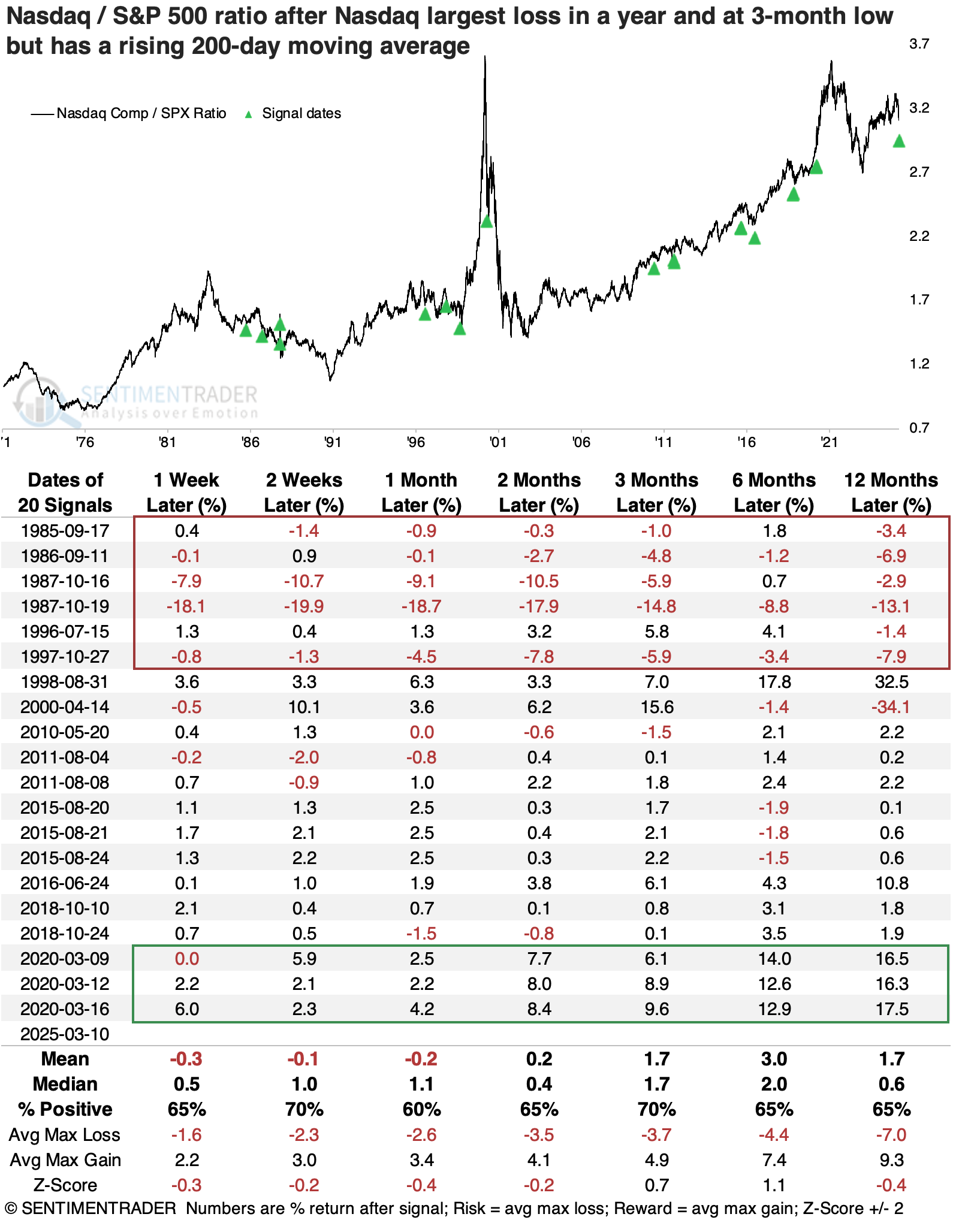

When we look at the ratio of the Nasdaq Composite to the S&P 500, we can see how the former has dominated the latter over the decades. But these Nasdaq mini-shocks tended to precede less outperformance for the Nasdaq. That was especially true before the lead-up to the internet bubble. Since then, the ratio has mostly preceded only modest outperformance, if any, for the Nasdaq in the months ahead. The stimulus-fueled rocket ride after the Covid pandemic was one of the few exceptions.

The summary stats below show how the averages change when we exclude just those three signals from 2020.

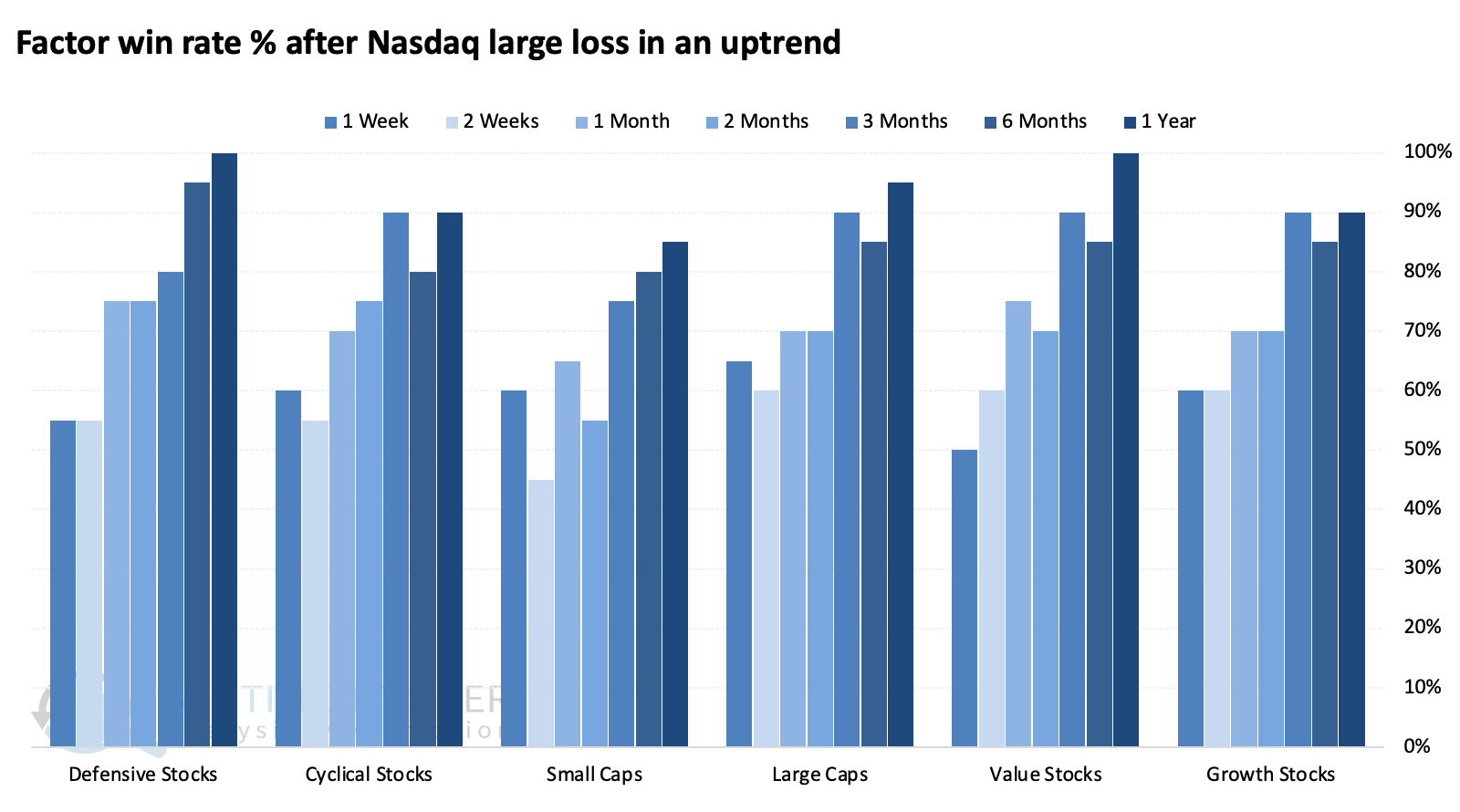

As we've seen with so many studies in recent weeks and months, these signals tended to favor defensive factors over more cyclically aligned ones. The defensive factor showed the highest one-year returns and significantly more consistency in positive returns.

What the research tells us...

A market, or index, that's mostly dominated by momentum-chasing traders tends to perform poorly when that momentum leaves and dip-buyers show no interest in returning. There is nascent evidence that this is the case in the Nasdaq 100, and it bears watching in the coming weeks. Already, the signs aren't encouraging there.

But that doesn't necessarily have as much impact on broader indices or those that tend to hold higher-quality and/or more diversified companies. Short-term risk was relatively high, but after investors got their nerves settled, medium- to long-term returns were consistently above average.