This breadth signal suggests a pause

Key points:

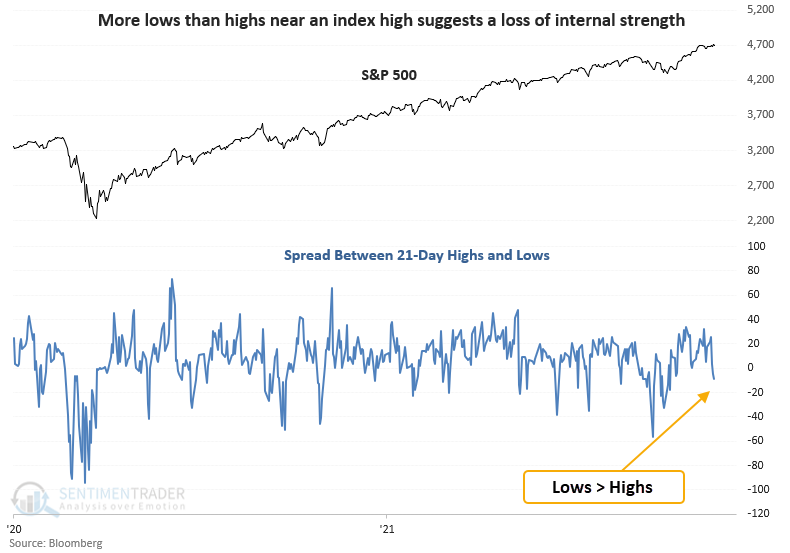

- New lows are greater than new highs, with the S&P 500 near a high

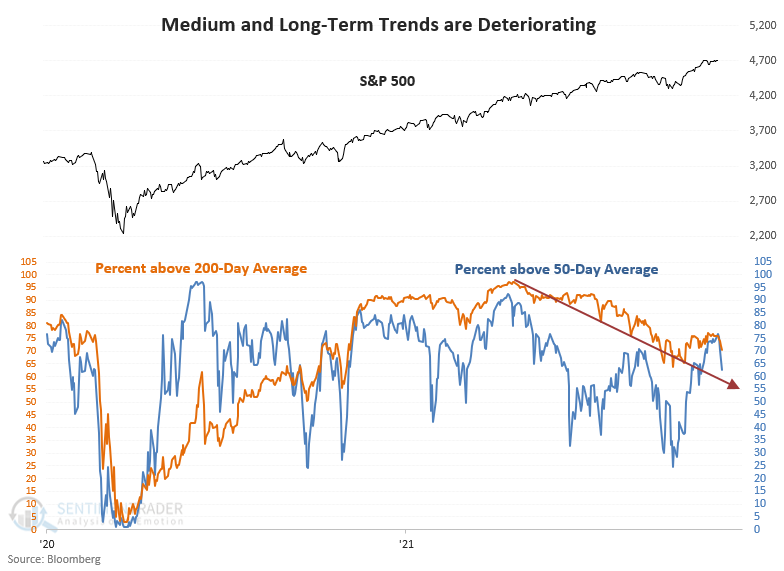

- Medium and long-term stock trends are deteriorating

- Similar conditions preceded negative returns in the near term

Several breadth indicators suggest the market is losing internal momentum

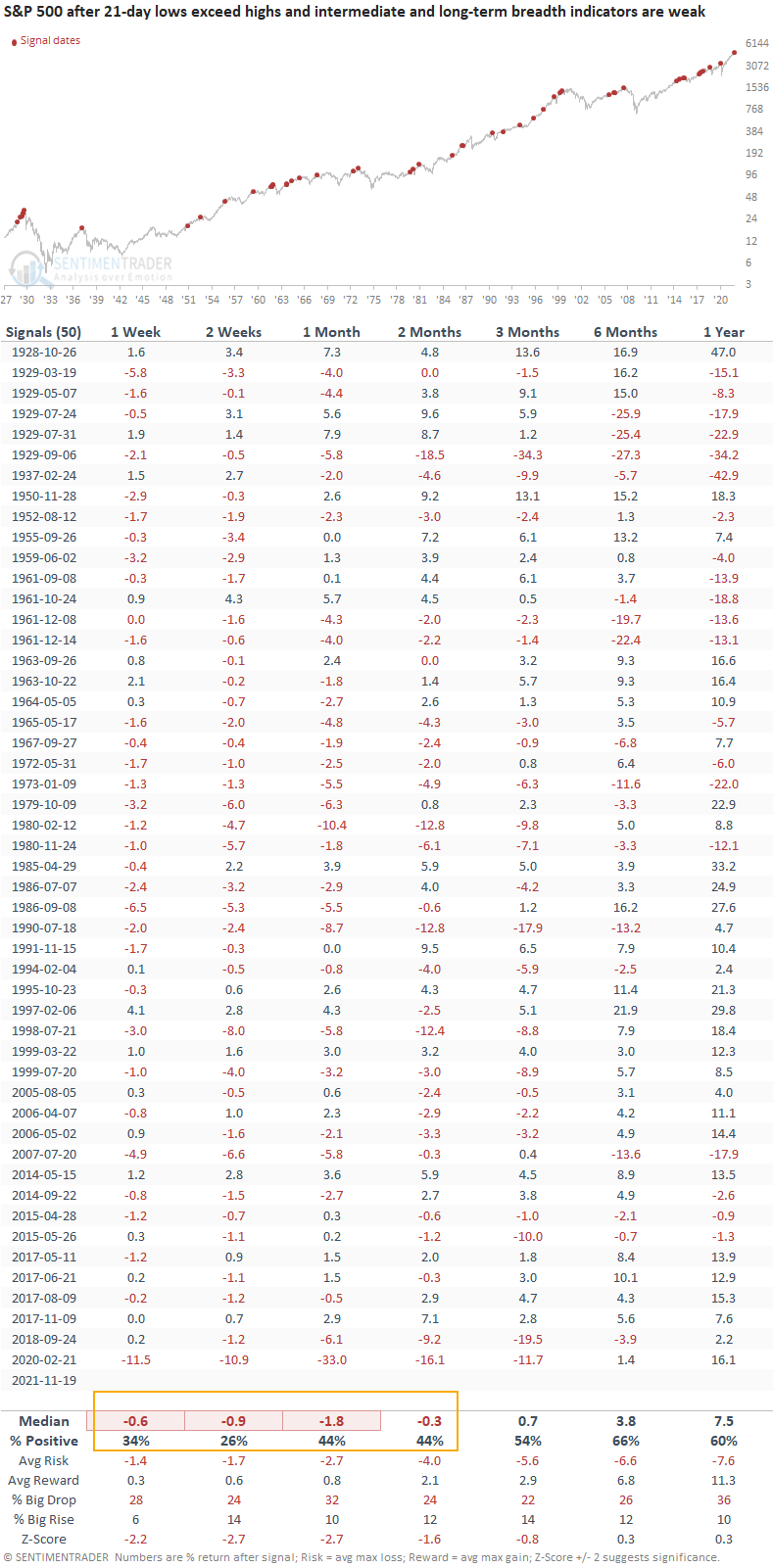

A new signal from a voting member in the composite risk-off model issued an alert on Friday. The component is called the New High Low Spread with Weak 50 & 200-day Average model.

If you were wondering, the model requires the following criteria to issue an alert.

- S&P 500 <= 2 days from a 252-day high

- The spread between S&P 500 21-day highs and lows are < -0.5%

- The percentage of S&P 500 members above the 50-day average < 66%

- The percentage of S&P 500 members above the 200-day average < 75%

The spread between the percentage of members at a 21-day high versus low turned decidedly negative on Friday, two days removed from an all-time high.

Medium and long-term stock participation trends have been trending lower for the last 6 months.

Similar signals preceded weak returns in the near term

This signal has triggered 50 other times over the past 93 years. After the others, future returns and win rates were weak in the short term with several unfavorable risk/reward profiles.

What the research tells us...

When 21-day lows exceed highs, and the percentage of members above the 50 & 200-day average are weak, stock participation is losing momentum. Similar setups to what we're seeing now have preceded weak returns and win rates in the short term. However, as we've seen all year, the unhealthy breadth conditions have generally been more indicative of rolling internal sector corrections associated with the latest Covid case count. When case counts start to rise, money flows out of cyclical sectors and moves to the perceived safety of a few mega-cap technology stocks.