Nasdaq analogs show rising probability of higher prices

Key points:

- Over the past 6 months, the Nasdaq Composite has the "feel" of 1998, but objectively not so much

- The highest-correlation 6-month periods saw a few severe declines going forward, but most of them rose

- Using one-year analogs, the precedents to the past year mainly saw positive returns going forward

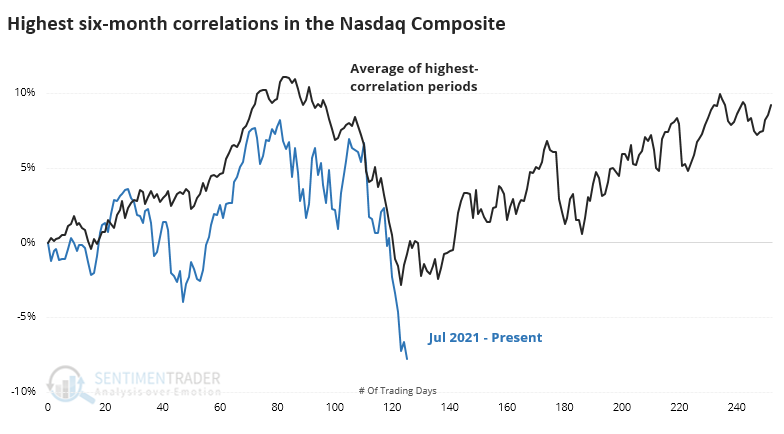

The periods most like the last 6 months

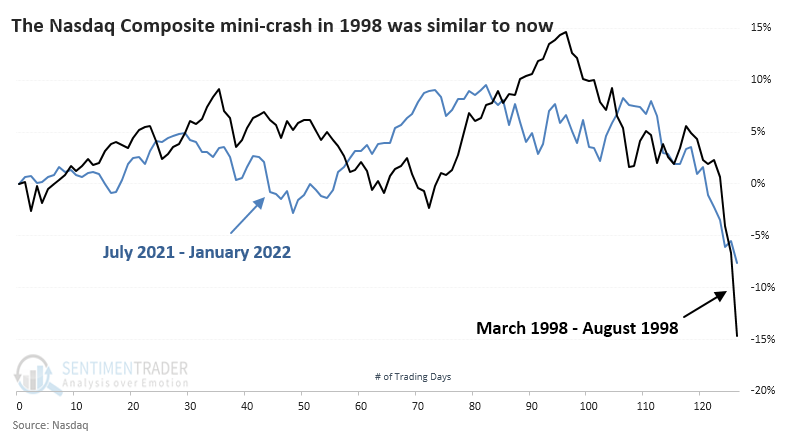

Trading activity over the past week has the feel of 1998 when stocks suffered a mini-crash. The Russian connection from then (they devalued the ruble) and now is coincidental. It's more that the price moves have a similar feel. I distinctly remember the panic our margin clerks felt when unable to reach clients who were under their equity requirements, and it's not hard to imagine similar feelings happening this week.

The charts are relatively similar, at least in that the Nasdaq went up, then down quickly.

We've learned over and over again over the years that memories and eyeballs can be deceiving. Just because the price action feels similar doesn't mean it necessarily was.

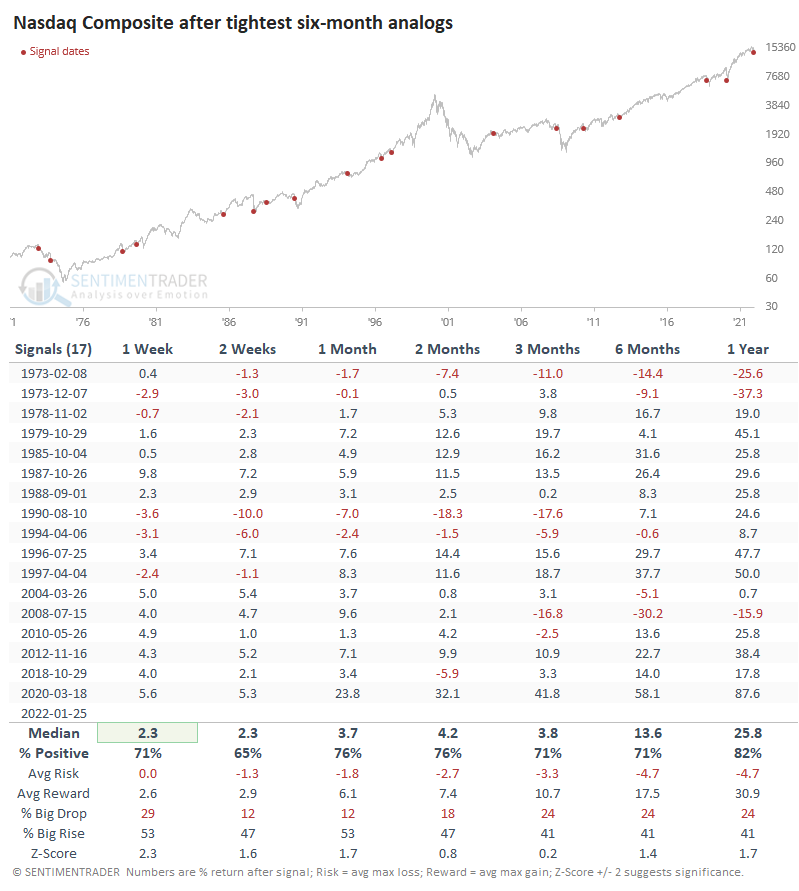

When we use our objective analog calculations to search for the highest-correlated periods since the Composite's inception in 1971, the year 1998 doesn't show up on the radar. It was close but didn't make the cut of highest-correlated 6-month analogs.

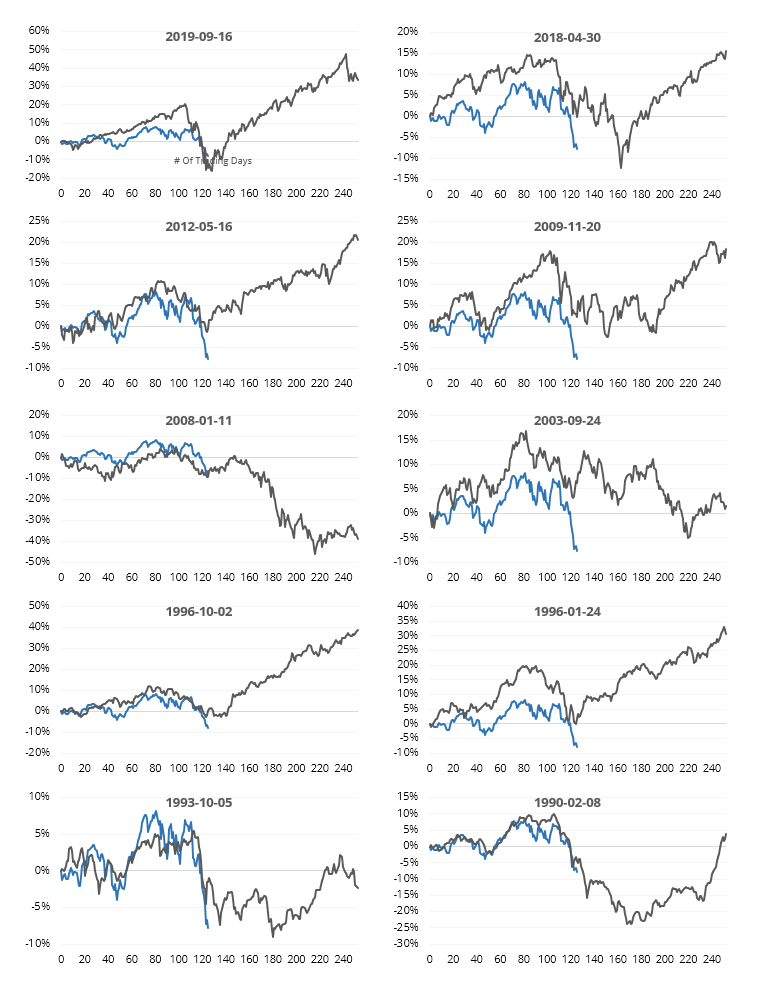

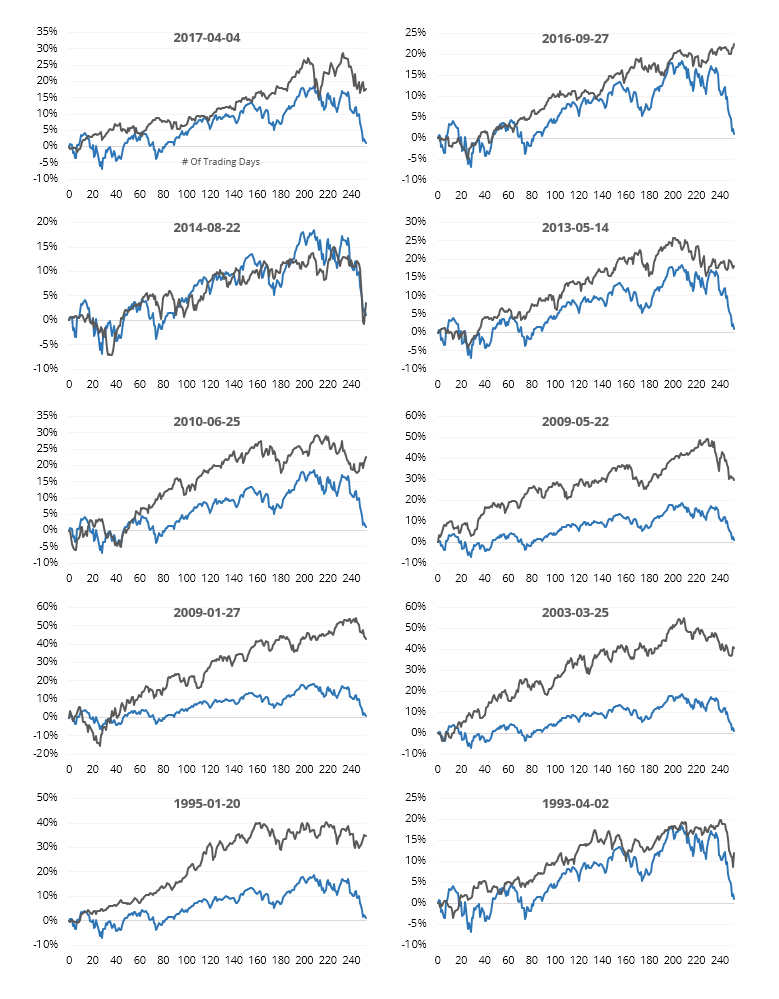

Thumbnails of the 10 most recent signals are shown below.

We're less interested in charts that happen to look alike and more interested in what they indicated for future performance. In that sense, it was mostly positive...except when it wasn't, and the Nasdaq crashed harder. Similar price behavior happened right before the Nasdaq lost another 10% or more within the next 3 months in 1973, 1990, 2008, and 2018. Those were the outliers, though, as the more common outcome was a lasting rebound.

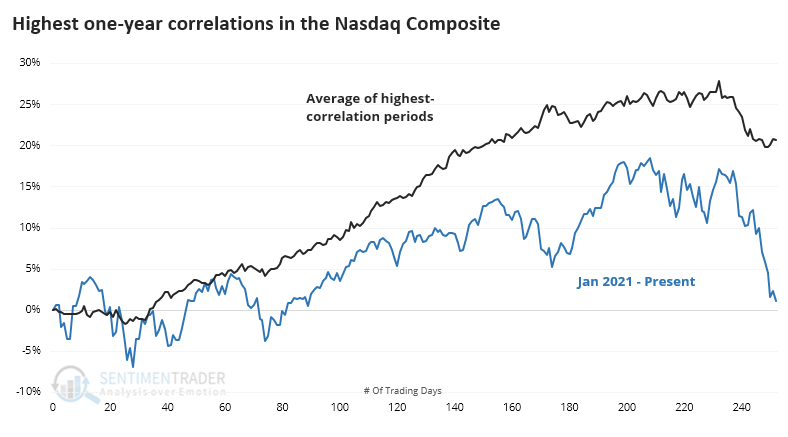

Extending the time frame to one year

Maybe our comparisons will change if we extend the time frame. Instead of 6 months, the analogs below look at the tightest one-year patterns. By definition, these were years (using trading days, not calendar dates) when the Nasdaq Composite rose for months on end and then usually saw a significant retracement.

Because much of the past year was dominated by a rising trend, it's no surprise that quite a few recent years show up in the correlations.

Again, we're more interested in future returns. And again, those were mostly positive. There was less chance of a significant decline in the months ahead; over the past 30 years, all showed a positive one-year return.

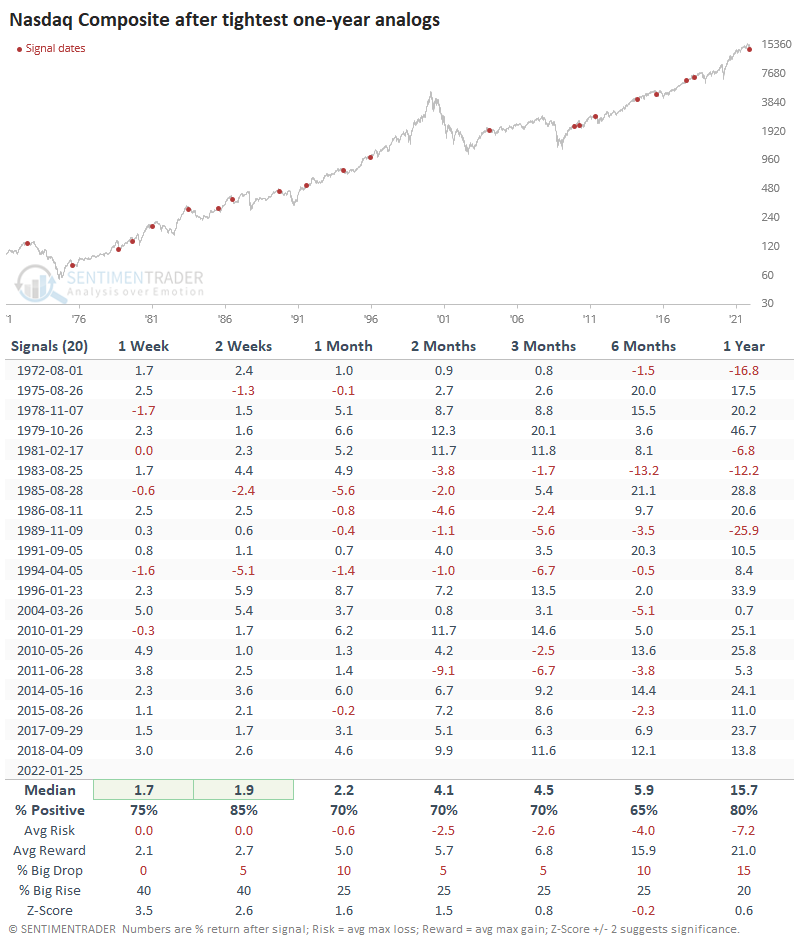

What the research tells us...

Using price analogs is fraught with danger, as it's too easy to cherry-pick some charts that kind of look like the recent past. Using a more objective process has been helpful over the years, and when we do that, there are a few scary precedents but mostly positive outcomes. We wouldn't rely on analogs as a primary factor when weighing the evidence of risk vs. reward, but we'd consider a small addition to the "reward" side of the ledger.